Rising Focus on Crop Yield Protection Drives SDHI Fungicide Market Expansion Toward 2036

According to Fact MR's latest analysis, Driven by escalating global crop disease pressures and a structural shift toward program-led resistance management, theglobal Succinate Dehydrogenase Inhibitor (SDHI) fungicide market is entering a high-growth phase. Fungal pathogens threaten crop yield quality across both broadacre and horticulture crops, forcing growers to adopt advanced preventive chemical measures. According to latest industry intelligence, the global adoption of SDHI formulations is accelerating rapidly, moving from traditional reactionary sprays to structured, mixture-based rotational protocols required by the Fungicide Resistance Action Committee (FRAC).

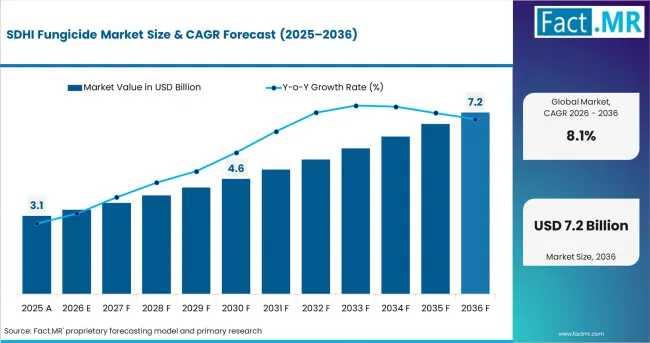

Executive Summary & Stakeholder Insights

Valuation Trajectory: The global SDHI fungicide market stood at USD 3.1 billion in 2025, is valued at USD 3.3 billion in 2026, and is projected to expand to USD 7.2 billion by 2036.

Compounded Growth: The market will exhibit a highly robust CAGR of 8.1% during the 2026-2036 forecast window.

Cereal Dominance: The grains and cereals application segment dictates market direction, capturing a 39.0% market share in 2026 due to intensive leaf and ear disease control in wheat and barley crops.

Formulation Innovation: Suspension concentrates represent the preferred delivery method, commanding a 43.0% market share in 2026 due to the operational requirement for stable liquid dispersion during high-volume tank mixing.

Operational Delivery: Foliar spray remains the dominant treatment mode, expected to hold a 61.0% market share in 2026, enabling real-time, in-season response to atmospheric disease outbreaks.

Supply Chain Mechanics: Distributor supply networks command a 46.0% market share in 2026, acting as the critical link for combining localized product availability with agronomic field advice.

Regional Growth & Primary Catalysts (2026-2036)

India (9.1% CAGR): Expanding horticulture production and a rapid transition to structured, program-led crop protection for rice and vegetable crops are accelerating demand, heavily supported by an increasing localized distributor footprint.

China (8.8% CAGR): Growth is sustained by an immense broadacre crop footprint, high native pesticide formulation capacity, and deeply integrated, steady preventive application cycles within large-scale commercial cereal farming operations.

Brazil (8.6% CAGR): Persistent high-humidity environmental conditions continue to drive extreme foliar disease and rust pressures across massive broadacre soybean and cereal acreages, forcing reliance on premium chemical protection.

United States (8.2% CAGR): Deeply integrated ag-retail distribution networks and a high baseline adoption rate among growers for advanced, systemic SDHI actives ensure steady volume growth across major grain producing states.

Germany (7.6% CAGR): A highly sophisticated regulatory landscape mandates strict compliance with chemical rotation and resistance management protocols, keeping baseline demand high within established wheat and barley programs.

Competitive Landscape & Entity Mapping

BASF SE (Estimated Market Share: 22-26%)

Market Strategy: Dominates via established broad-spectrum active ingredients, notably utilizing its Endura PRO label (listing boscalid as a Group 7 fungicide) to cement market share in potato and broadacre crop disease sectors.

Bayer AG (Estimated Market Share: 18-22%)

Market Strategy: Targets high-value horticulture and arable crop segments through its advanced fluopyram active chemistry portfolio, prioritizing combined fungicide and nematicide technical features.

Syngenta AG (Estimated Market Share: 17-21%)

Market Strategy: Expands broadacre market presence through premium fluxapyroxad and proprietary SDHI co-formulations engineered specifically for early-stage cereal protection.

Corteva Agriscience (Estimated Market Share: 11-15%)

Market Strategy: Leverages extensive retail distribution alignments and bundled seed-and-crop-protection portfolios to lock in long-term supply contracts with multi-state farming operations.

Segment-Wise Performance

By Active Ingredient Type

Boscalid: Holds the leading market position with an estimated 28.0% market share in 2026. This dominance stems from its deeply established registration footprint, widespread cross-crop labeling, and proven baseline efficacy among growers.

Fluopyram: Functions as a high-margin growth engine, capturing market share within specialty vegetable, fruit, and premium orchards.

Fluxapyroxad: Gains rapid market volume by anchoring preventative spray programs across modern, high-yield cereal rotations.

By Application

Grains & Cereals: Commands a dominant 39.0% market share in 2026. High leaf and ear disease exposure during critical reproductive growth stages necessitates multiple planned applications of SDHI chemistries per season.

Oilseeds: Expands steadily as soybean and canola producers scale up chemical protection measures to safeguard crop yields against aggressive rust and foliar blights.

Fruits & Vegetables: Represents a key value driver, where SDHI application focuses on ensuring external fruit appearance and preserving saleable retail characteristics.

By Formulation

Suspension Concentrates (SC): Captures 43.0% market share in 2026. Commercial growers favor SC formulations due to their ease of liquid tank handling, stability in solution, and uniform crop coverage.

Seed Treatment Formulations: Experiencing rapid long-tail keyword growth as the industry shifts toward preventative, early-season systemic protection before foliar pressures peak.

Direct Q&A Section

What is the projected global SDHI fungicide market size by 2036?

USD 7.2 billion is the projected valuation of the global market by 2036. The market will expand from its 2026 valuation of USD 3.3 billion, registering a steady compound annual growth rate of 8.1% over the ten-year forecast window.

Which country exhibits the fastest growth rate in SDHI fungicide demand?

India is the fastest-growing market, expanding at a projected 9.1% CAGR from 2026 to 2036. This rapid growth is driven by expanding horticulture production, escalating crop disease pressures, and a national transition toward program-based crop protection strategies.

Why do suspension concentrates dominate the formulation segment?

43.0% market share belongs to suspension concentrates because large-scale commercial spraying requires stable liquid dispersion, simple tank handling, and uniform leaf coverage. Regulatory approvals, including the EPA's Zorina label, actively endorse this formulation format for structured preventative spraying.

What is the primary operational challenge facing SDHI fungicide manufacturers?

Fungicide resistance stewardship is the main challenge. SDHI chemistries possess a single, highly specific mode of action targeting fungal respiration; consequently, manufacturers must actively mandate partner chemistries and complex rotational spray programs to prevent target pathogens from developing chemical immunity.

About Us

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.