SiC Power Semiconductor Market Share: The Competitive Battle for High-Voltage Dominance

The SiC Power Semiconductor Market Share is currently the subject of intense competition between legacy semiconductor giants and specialized boutiques. Unlike the traditional silicon market, which is largely commoditized, the SiC space rewards companies that can master the difficult "Crystal Growth" phase. As a result, market share is highly concentrated among a few players who have secured long-term supply agreements for raw SiC substrates, making the "Upstream" part of the business the real battlefield for dominance.

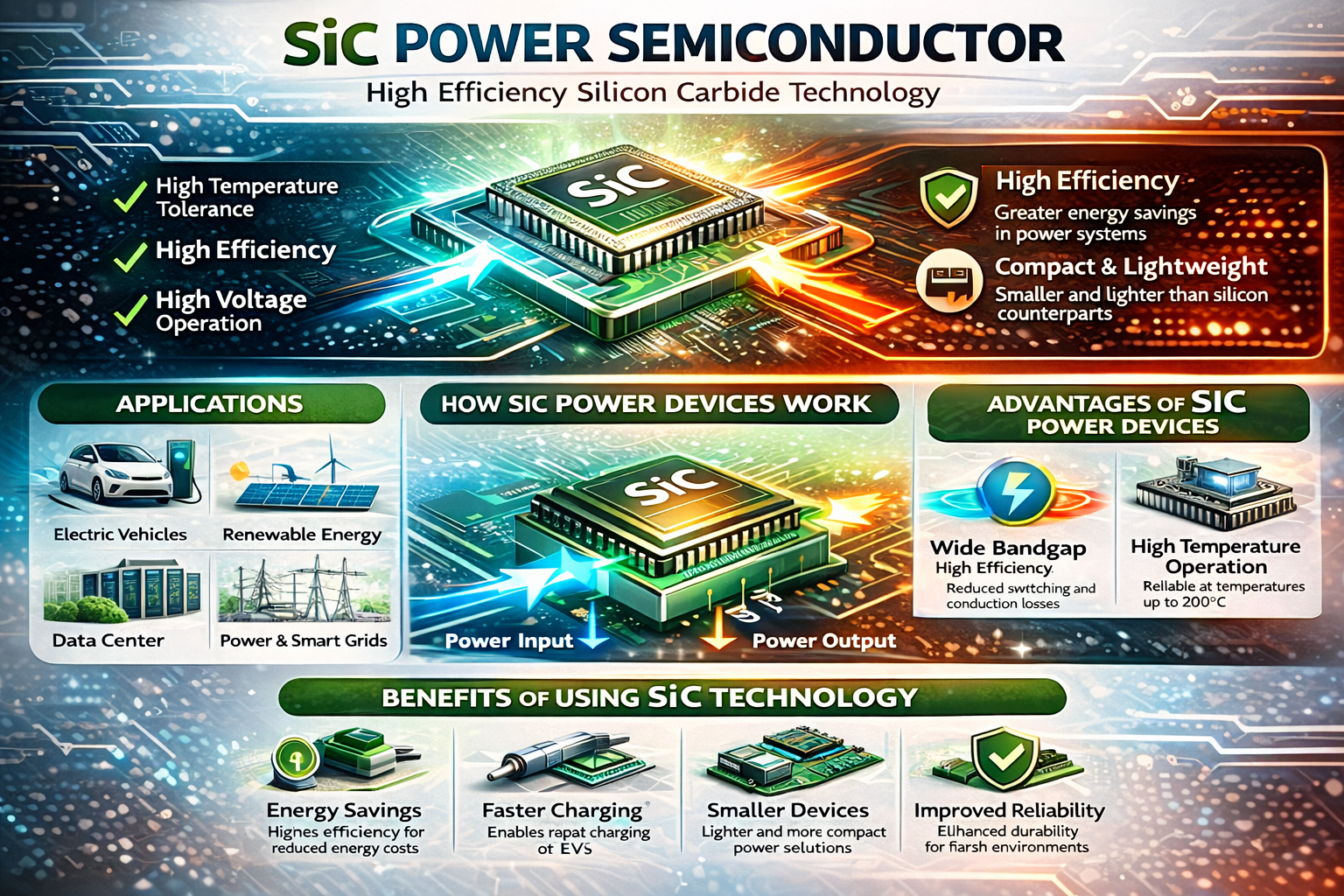

Market Overview and Introduction

The battle for market share is being fought across the SiC power devices landscape, from simple diodes to complex MOSFETs. Companies that can provide high efficiency power modules that are "Plug-and-Play" for EV manufacturers are currently gaining the most ground. This shift is forcing traditional power electronics firms to acquire SiC startups or risk losing their position in the rapidly evolving automotive supply chain.

Key Growth Drivers

The primary driver for shifting market share is "Vertical Integration." Companies that own the entire process—from growing the SiC boule to slicing the wafer and fabricating the chip—have a massive advantage in cost and quality control. Furthermore, the "Design-In" cycle for automotive and industrial products is very long; once a company wins a spot in a vehicle's drivetrain, they are virtually guaranteed market share for the life of that car model, leading to fierce competition for current contracts.

Consumer Behavior and E-commerce Influence

While the "End Consumer" doesn't buy SiC chips directly, their preference for brands that represent "Innovation" and "Sustainability" forces OEMs (Original Equipment Manufacturers) to choose the best components. This has led to a "Tier 1" effect, where a few semiconductor brands have become synonymous with high-quality SiC technology. E-commerce and digital catalogs have also played a role, as they allow engineers to easily identify which manufacturers have "Stock on Hand," a critical factor during the ongoing global supply chain fluctuations.

Regional Insights and Preferences

Japan currently holds a significant portion of the IP-based market share, with its firms leading in specialized manufacturing equipment. However, European firms have a strong grip on the industrial and energy grid market share. The United States is home to several of the world's largest SiC substrate producers, giving it a strategic advantage in the "Raw Material" layer of the market. China is aggressively using state subsidies to build its own domestic ecosystem, aiming to capture 100% of its internal market share by 2030.

Technological Innovations and Emerging Trends

One disruptive trend is the move toward "Fab-Lite" models, where companies design the chips but outsource the difficult fabrication to specialized SiC foundries. This allows more players to enter the market without the multi-billion dollar cost of building a cleanroom. We are also seeing a trend toward "Packaging Innovation," where chips are embedded directly into the circuit board to further improve thermal performance, a move that is reshaping how companies compete on a "System Level" rather than just a "Chip Level."

Sustainability and Eco-friendly Practices

Market share is increasingly tied to "Green Audits." Large corporate buyers now demand that their semiconductor suppliers prove their manufacturing processes are as low-impact as possible. Companies that use renewable energy to power their energy-intensive SiC furnaces are gaining a "Sustainability Premium" in the eyes of their customers, allowing them to capture market share from less eco-conscious competitors.

Challenges, Competition, and Risks

The primary risk for market leaders is "Technological Leapfrogging." If a competitor discovers a way to produce SiC wafers twice as fast or with zero defects, current market share could evaporate overnight. There is also the risk of "Overcapacity"; as everyone builds new fabs at the same time, the market could eventually see a price collapse if demand doesn't keep pace with the massive new supply expected to come online in the next three to five years.

Future Outlook and Investment Opportunities

The future outlook for market share is one of "Consolidation." Expect to see more M&A (Mergers and Acquisitions) as the "Big 5" semiconductor firms look to buy out smaller competitors to consolidate their hold on the raw materials. For investors, the "Equipment Makers"—the companies that sell the specialized saws and polishers needed for SiC—are the "Picks and Shovels" play that benefits no matter which chipmaker eventually wins the market share war.